Chris Hayes had Gene Sperling, Director of the National Economic Council for President Obama, on while guest-hosting the Last Word with Lawrence O’Donnell last night. Hayes played the clip that Krugman recently highlighted, where Obama said that the government’s budget is like a family’s budget that has to tighten in hard times and emphasized deficit reduction as a means to get confidence going to kick up the recovery, and asked Sperling to explain. Hayes also brought up the historical-low interest rates on Treasuries as a counter-argument to these points.

You’ll be happy to know that Sperling brought up that the government is, in fact, kind of like a family, that trillions on corporate balance sheets are a little bit because of a lack of confidence, especially on the deficit, and, my favorite, this, in response to Hayes bringing up the interest rate as the most sophisticated pricing instrument we have on government debt:

“well I think there’s a lot of factors that go into the interest rates right now. But there’s certain things you know that are just sound….any country anywhere that has its debt increasing as a percentage of its income creates doubts about its sustainability. That’s gotta discourage some people from feeling as good as the long-term investments…”

Wow. It is quite funny to watch Hayes’ jaw drop with a sense of horror when he realizes what he’s hearing from one of the key current architects of the Democratic economic platform:

I’m pretty up-to-date on the conservative arguments for expansionary austerity, from data to assumptions to talking points, and what Sperling is saying is more or less indistinguishable from the latest round of right-winger talking points.

It also appears, God bless ‘em, that the administration is going to start rotating structural unemployment talking points in their discussion of the economy as well. So, what gives? Why has the administration gone this route? This is different than the idea that they don’t want to be associated with the stimulus or further efforts at stimulus – this is running into the exact opposite arguments.

Krugman thinks it’s because the Very Serious People embrace this and Obama is wired to think that VSP know what the right course of action is. That sort of restates the question, which is why do VSP and Obama’s immediate economic team embrace this argument? I can think of a few guesses.

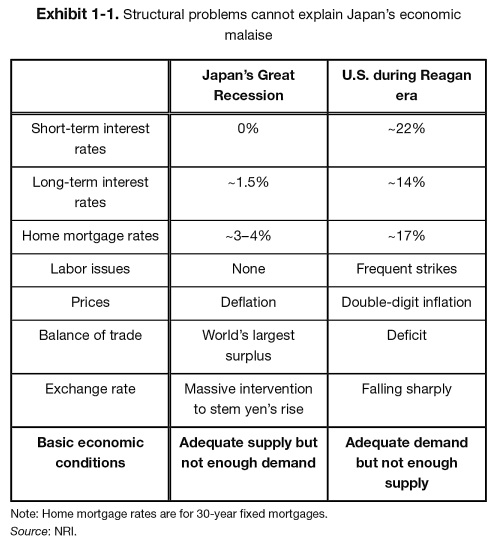

The 1980s

Richard Koo is an expert on the Japanese recession who calls for continued aggressive fiscal stimulus in the United States. In his recent book, The Holy Grail of Macroeconomics, he makes an early point to explain how he though there were serious structural problems in the late 1970s and early 1980s, and supported the “reforms” necessary to break it. Reading it, it is clear that he thinks making this point establishes his ability to call out a demand recession, because he is equally unapologetic in calling out a supply recession. He made this chart that explains what he saw in Japan versus the Reagan U.S., and also concludes that we look like the Japan scenario:

If you are someone who idolizes Reagan, or thinks the early 1980s gave us the answers that are everywhere and anywhere applicable (a phenomenon that now goes beyond tax cuts for everything), or sees severe debt-deflation and a minimum wage side-by-side and thinks the minimum wage is, far and away, the more ghastly thing you are seeing, if you are someone who never got over the 1980s or understood that there’s an alternative, it doesn’t surprise me that you would be find this logic convincing.

The 1990s

Felix Salmon noted the following about ideology and job creation when the whole stimulus as “sugar” debate happened:

Geithner cut his teeth in a world of bond vigilantes, an era when James Carville said that he would like to be reincarnated as the bond market, because then he could intimidate everybody. And after that, Geithner dealt with a series of international sovereign-debt crises where countries found themselves hammered by enormous bond spreads.

The people in the senior economic policy shop are primarily Wall Street people, who view the world in a much different frame that those looking at demand-side, deflationary consumer pressures. Similarly they are people who think that a solid Wall Street will be the driver of the economy, an argument we’ve seen going back to at least PPIP.

Also the 1990s is when neoliberals really took over the macroeconomic arguments (see this Galbraith argument). Liberals abandoned demand-side arguments in order to try and win over a role for the government in the supply-side arguments – the liberal government can bring job training, relocation loans, tax credits, etc. to help with employment, leaving the demand side arguments to disappear.

Meritocracy, Rentiers

The most stable, and the least easily shifted, element in our contemporary economy has been hitherto, and may prove to be in future, the minimum rate of interest acceptable to the generality of wealth-owners. If a tolerable level of employment requires a rate of interest much below the average rates which ruled in the nineteenth century, it is most doubtful whether it can be achieved merely by manipulating the quantity of money.

Certainly our housing policy is being run on the idea that homeowners should eat as much of the costs as they can potentially bear, even if it means keeping the economy depressed for years longer than it needs to be. Stimulus, a short-round of inflation and bad-debt writedowns all would help the economy, but all hurt rentiers. Right now Wall Street has a great deal milking the remains of the housing bubble’s bad debts.

When these are the smartest, most meritocratic guys in the room, it is perfectly designed for acceptance from Very Serious People, especially creations of the meritocracy like Obama.

These are all idle speculations. Your thoughts?

No comments:

Post a Comment